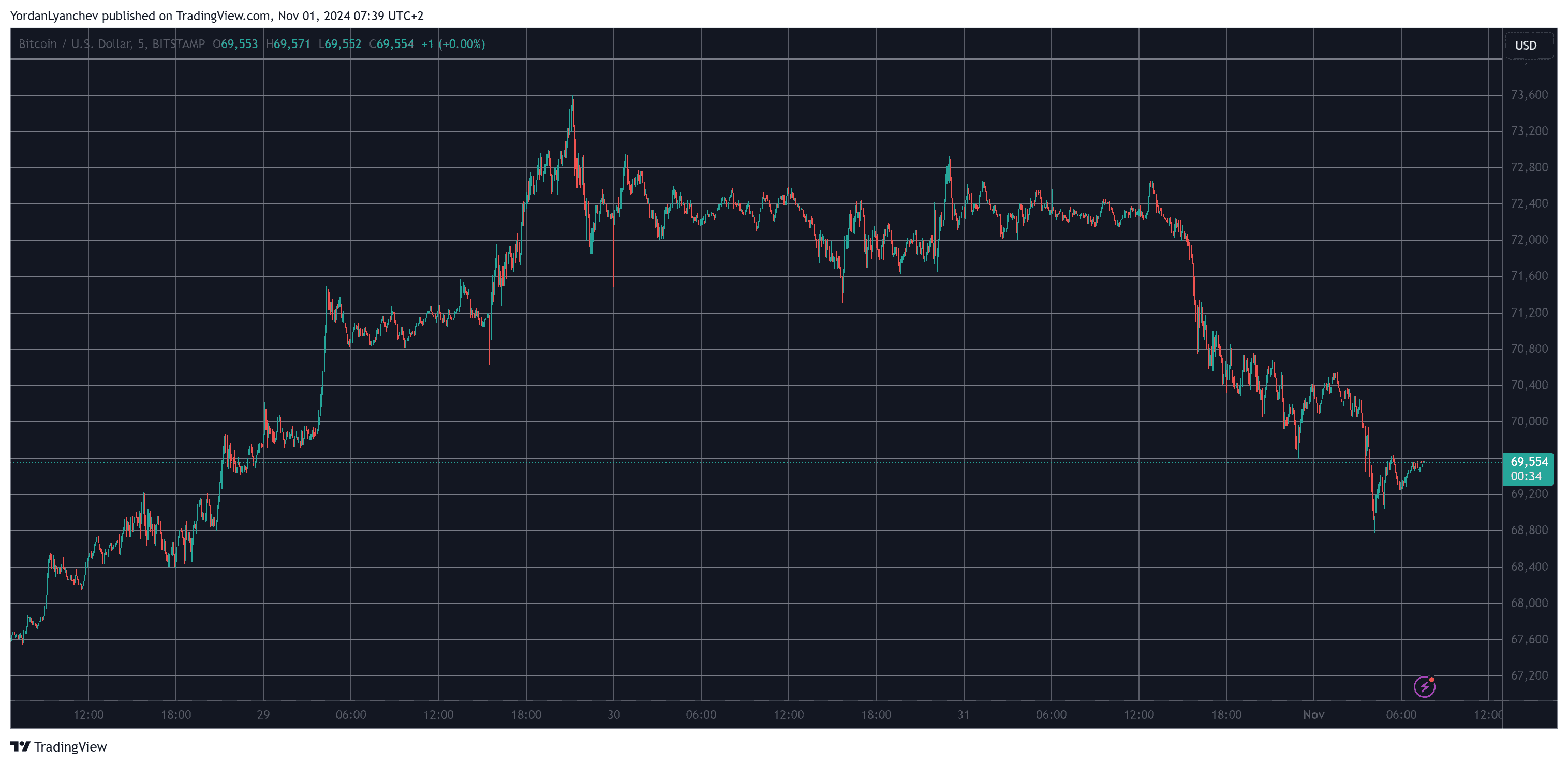

BTC’s inability to break its own all-time high has resulted in a massive rejection that pushed it south hard to under $69,000 earlier today.

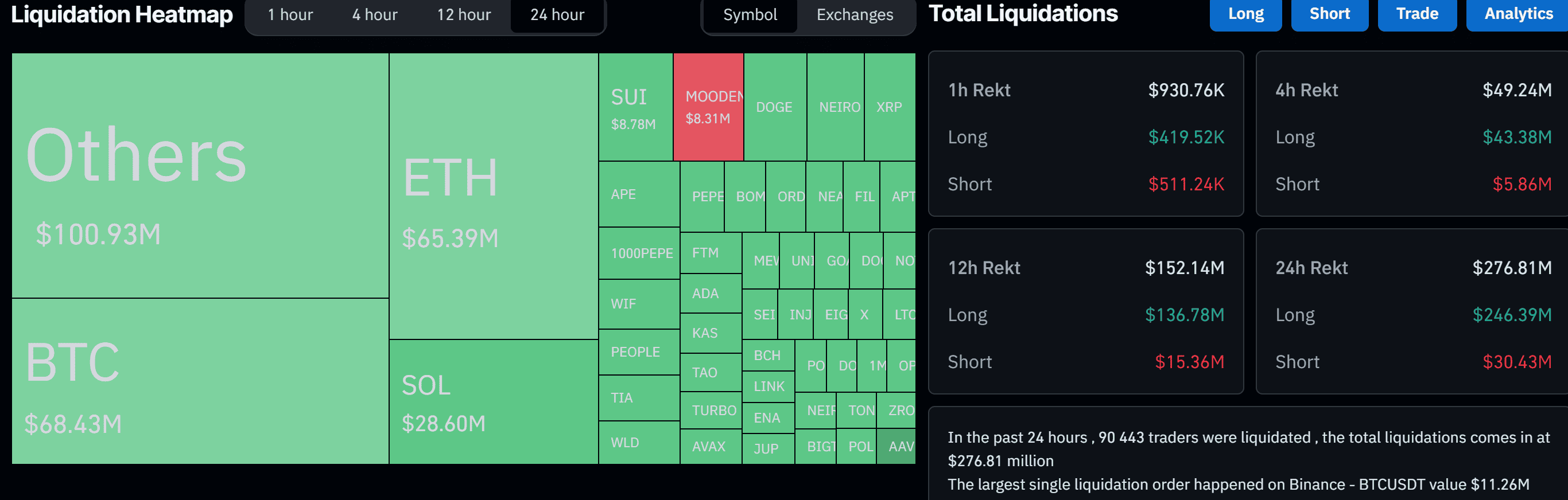

The altcoins have followed suit, which has harmed over-leveraged traders, with more than 90,000 such market participants getting wrecked in the past day.

The primary cryptocurrency was on a roll this week, perhaps driven by the massive net inflows into the 11 US-based spot Bitcoin ETFs. As reported yesterday, October 30 was the second-best day for the financial products in terms of net inflows since their inception in mid-January.

The rally culminated on Tuesday with a surge to $73,600, which meant that bitcoin had come just $150 away from tapping a new all-time high.

While the community was expecting this to occur at any moment, BTC retraced slightly to $72,000 on Wednesday and Thursday before it dumped hard hours ago.

It went from the aforementioned level to under $69,000 in minutes, losing over three grand in the process. As of now, it has recovered some ground, but it is still well below $70,000.

Many altcoins have suffered even more in the past day, with ETH and SOL dumping by 5% each. The two largest meme coins – DOGE and SHIB – have slumped by 7.5% and 6.2%, respectively.

The cumulative market cap of all crypto assets is down by approximately $100 billion since yesterday and is beneath $2.450 trillion now.

This enhanced volatility has resulted in more than 90,000 traders being wrecked in the past day. The total value of liquidated positions is up to $280 million, according to CoinGlass. The single-largest wrecked position took place on Binance and was worth over $11 million.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER 2024 at BYDFi Exchange: Up to $2,888 welcome reward, use this link to register and open a 100 USDT-M position for free!

Source link

{kind=link}