Bond market liquidity was so 2010s. Nowadays, stock market concentration is the new trendy bugbear of finance.

Worries are understandable. After all, it’s hard not to feel at least a little bit uneasy about the phenomenon, which is remarkable across three dimensions: size (big is better than small); industry (tech über alles) and geography (America First).

There are a multitude of ways to show these interlocking facets of concentration. The most popular one is simply to calculate how much of the S&P 500 index the top 10 members account for. At the moment that stands at a modern-day record of 37.3 per cent.

However, for Alphaville the most arresting stat — via S&P Dow Jones Indices’ Howard Silverblatt — is that just 26 stocks now account for half the entire value of the S&P 500 index.

That’s down from an already-low 36 at the end of 2023, and is the lowest number since at least 1980. In fact, it is probably the lowest ever since the benchmark’s creation in 1957, though we’ve struggled to find historical data on its composition going back that far.

That is astonishing, and potentially has a lot of implications. Apollo’s chief economist Torsten Sløk argues that there’s now a “diversification illusion” when buying the S&P 500, which is in practice just Nvidia in drag.

The bottom line is that buying the S&P 500 gives the impression that you are buying 500 different stocks and diversifying your investments. But the reality is that the high and growing concentration in the S&P 500 continues to be a major problem. In short, investors should ensure that their portfolio is not all levered to Nvidia earnings.

Even the clown prince of SPACs weighed in on this over the holidays, arguing that it was a “disaster” waiting to happen for anyone buying a now-precariously concentrated S&P 500 index fund:

This needs to be fixed or it will end in disaster.

Why?

Average Americans buy S&P 500 index ETFs, in part, because Buffett told them to. They were told they would pay very little and get diversification in the 500 best companies on earth to ride out storms.

But as… https://t.co/YEYhjvrSg7

— Chamath Palihapitiya (@chamath) December 28, 2024

Look, yes, unambiguously this kind of concentration is obviously not great. It makes the global stock market look like an inverted pyramid resting precariously on a few big and richly-valued American companies.

If they tip over then the damage will be severe and widespread. US stocks now account for a whopping 66.6 per cent of the MSCI All-Country World Index (fittingly, the number of the beast). Apple, Nvidia and Microsoft alone make up 13 per cent of the $78tn index.

Even if there is no disaster, the valuations commanded by this narrowing clutch of US super-stocks have grim implications for longer-term returns, according to Goldman Sachs’ David Kostin. Alphaville’s emphasis below:

The intuition is, with high concentration, the forward realized volatility is likely to be greater because it’s a narrow group of companies driving the index any portfolio, if you have a relatively few number of constituents, the return is going to be more volatile than in a broadly diversified portfolio. And investors are not being compensated because the valuation is not attractively valued for this expected higher realized volatility.

And the reason that we make that statement is the following. If you look at these leading stocks. They trade today with a negative risk premium. We have not seen that at all for 20 years. At 31 times earnings for these companies, the inverse of 31 times is about 3.2%. That’s an earnings yield. Look at 10-year U. S. treasury yields today, that’s like 4.2%. That’s a negative risk premium. You get a earnings yield that’s below the return that you can get on 10 year treasury yields. The rest of the market is trading at a positive risk premium. That’s one factor.

And then the second is these stocks that are driving that high concentration are trading at very high valuations because the expectation is their growth is going to be really, really elevated for a persistently long period of time going forward. 4 These companies are expected to have 20% growth going forward. But history shows that the number of companies that can actually deliver 20% growth year after year after year after year fades dramatically and almost no companies can continue to do that over a decade

However, it’s important to remember that a small minority of stocks will almost always dominate returns in any given year. And over time that is particularly true.

We hate to trot out Hendrik Bessembinder once more, but as his research has shown, most stocks actually lose money. In fact, only 2.4 per cent of 64,000 public companies listed across the world account for all the $76tn of net global stock market wealth created between 1990 and 2020.

Secondly, the US stock market is still actually less concentrated than the international norm, as Toby Nangle pointed out last year. And, depending on what you look at, US equities are less concentrated than in the 1950s, when the S&P 500 was born (at the time it consisted of 25 railway stocks, 50 utilities, and 425 industrial companies).

Moreover, while the AI frenzy has stirred a lot of valuation froth, the phenomenon is a long-term trend caused primarily by increasingly concentrated corporate profits. As Acadian Asset Management’s Owen Lamont said in a discussion with Goldman’s Kostin in December:

. . . Today’s high stock market concentration is mainly just a mechanical function or mechanical byproduct of the fact that mega cap growth firms have had incredibly high profit growth in the past 10 years. And that is the main story.

The second story is that growth firms, mega cap tech firms are somewhat more richly valued than they were 10 years ago. Put those two facts together, and you’ve got a more concentrated market. So if you want to worry about something, worry about those things, don’t worry about concentration.

Lamont uses the example of AT&T’s break-up as an example of how measures of concentration can be irrelevant to the stock market’s riskiness — being split up into seven smaller companies in 1984 made the market optically less concentrated, but no less risky.

The reality is that today, many big listed companies are pretty diversified pseudo-conglomerates. The likes of YouTube, WhatApp, AWS, Instagram, Apple’s app store, or Microsoft’s gaming division would probably be worth hundreds of billions of dollars if they were standalone listed companies. The main danger of concentration is that you’re overly exposed to the risks of just one company or sector going sour. With many modern US companies you are in practice getting exposure to multiple ones.

Most of all, the suggestion that it spells doom for investors — at least those who fecklessly plough their money into dumb cap-weighted indices — is questionable.

Yes, if the AI boom fizzles out then the top-heavy US stock market will tank, and so will global markets. Index funds will track the indices down. But the reality is that index funds will still end up doing much better than the average active fund manager.

Anti-passive zealots will often point out that index funds dumbly bought Enron or Lehman at their peak, or are now being forced into Tesla, Nvidia or MicroStrategy at eye-watering valuations. The correct response to that is: “So what?”

The reality is that the next Nvidia is probably already lurking somewhere in the US stock market, and that the alternatives are worse.

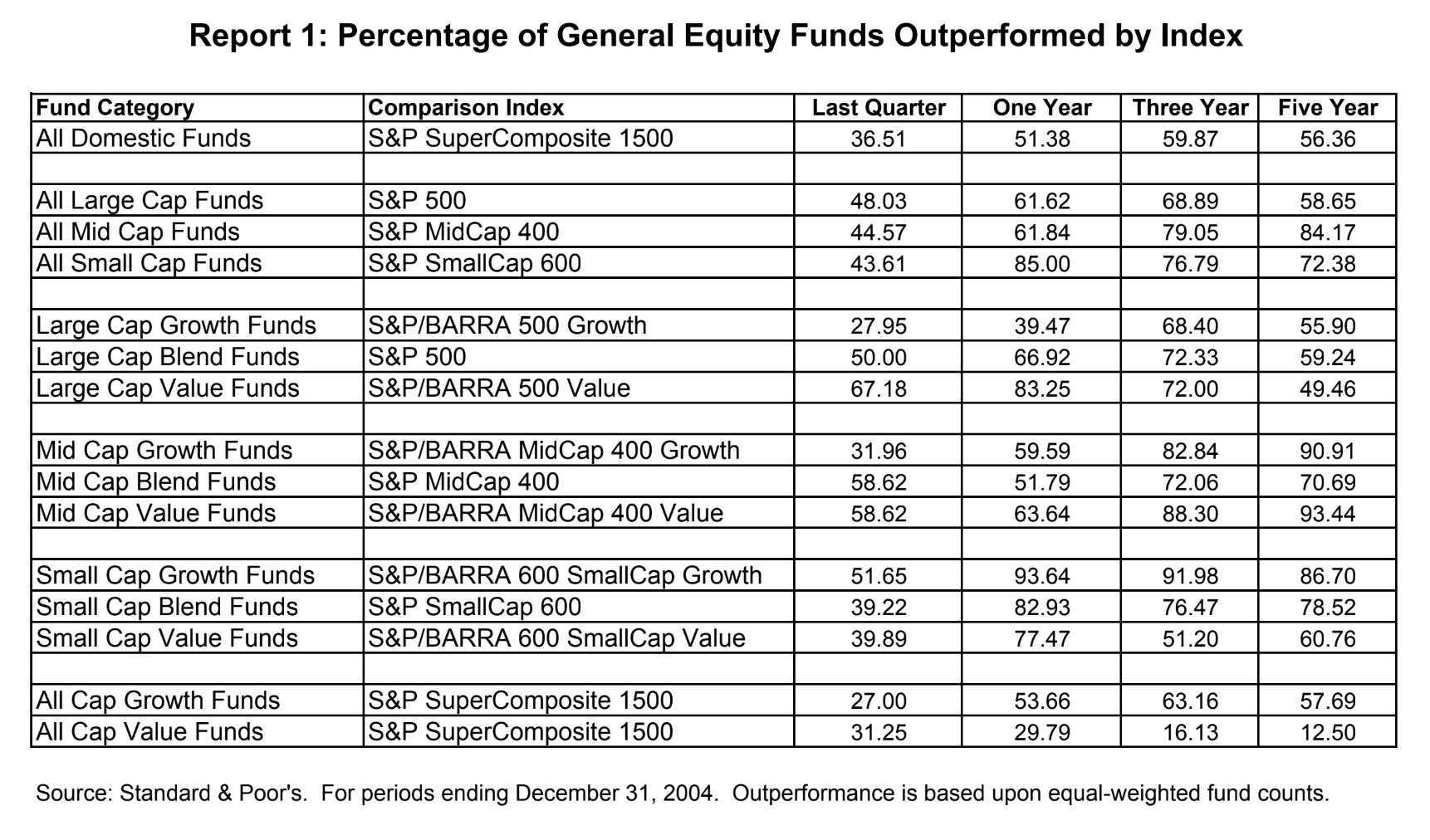

This is S&P Dow Jones’s scorecard for active versus passive performance from 2004, five years after the last time the US stock market was similarly bubbly and concentrated. As you can see, a majority of professional stockpickers still underperformed their benchmarks.

At the time the “SPIVA” scorecard only included five-year performance. In the subsequent five-year period stockpickers did even worse, leading to what would likely have been a grim 10-year period despite a supposedly great set-up at the end of 1999.

Sure, yes, if big US stocks tank then the US stock market will tank, and drag global equities down with them. Broad, capitalisation-weighted index funds will mechanistically suffer proportionate pain.

But concentration is in itself a poor gauge of the market’s riskiness, and the argument that extreme concentration means that you should therefore go with an active manager (or try to pick stocks yourself) is extremely weak sauce.

Further reading

— What’s your problem with stock market concentration? (FTAV)

— The interlocking dimensions of stock market concentration (FTAV)

{kind=link}